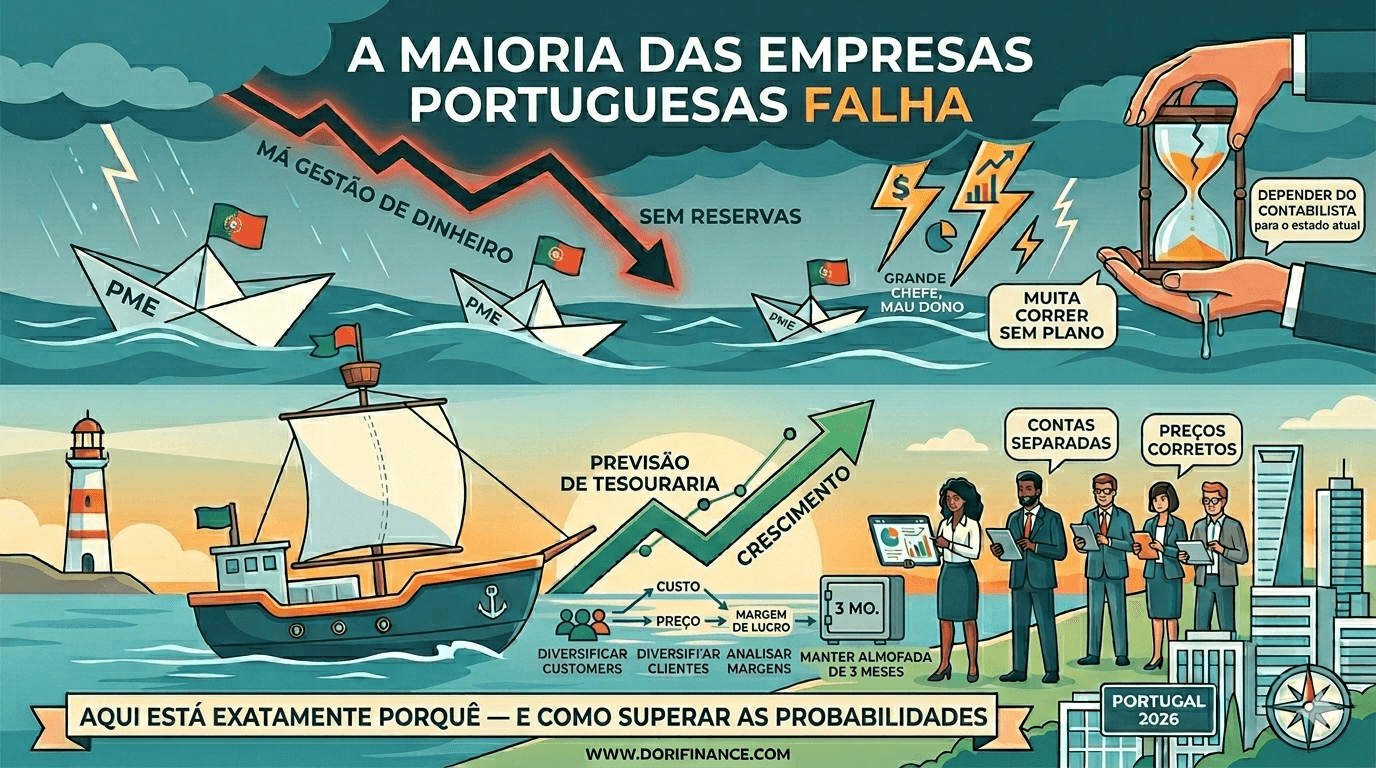

The Short Version

If you only read one page, read this one.

Small and medium businesses (SMEs) are the engine of Portugal’s economy. They make up 99.9% of all businesses in the country, provide the majority of jobs, and produce most of the national income. But there is a problem hiding behind those big numbers: most of these businesses do not last long.

Only about 3 in 4 new businesses make it through their first year. By year three, more than half have already shut down. That is a staggering number and in most cases, it was preventable.

The biggest reason businesses close is not a bad product, a bad location, or bad luck. It is poor money management. Owners run out of cash without seeing it coming. They do not know exactly how much money they are making or spending. They have no plan for a slow month or a difficult year.

This report explains what the data tells us about Portuguese businesses. In plain language, without complicated financial terms. It will show you why so many businesses fail, what mistakes to avoid, and what you can start doing today to protect yours.

1. How Many Businesses Are There in Portugal?

Let’s start with the basics: who are we talking about?

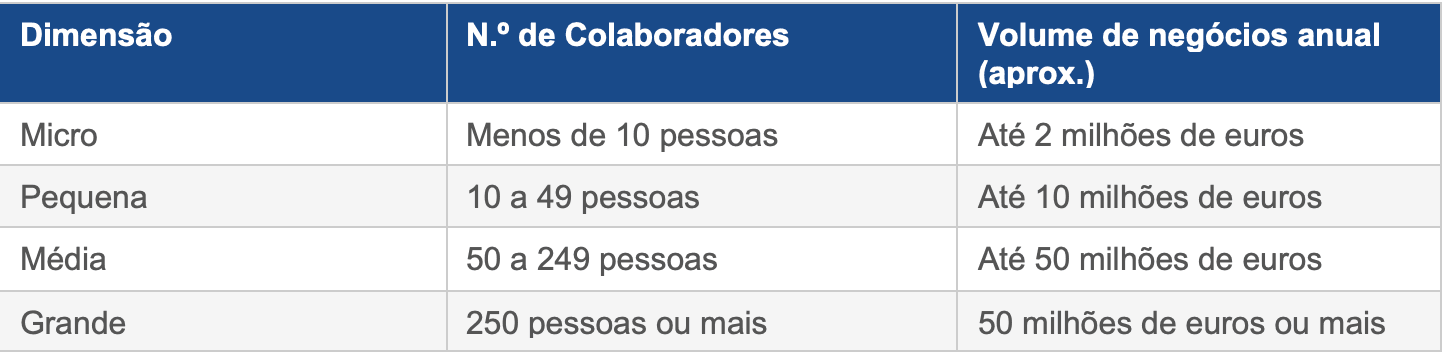

1.1 What counts as an SME?

An SME stands for “small or medium-sized enterprise”, basically any business that is not a large corporation. In Portugal and across Europe, businesses are grouped into four sizes:

The vast majority of Portuguese businesses are “micro”, tiny operations, often run by a single person or a small family team.

1.2 How big is the sector?

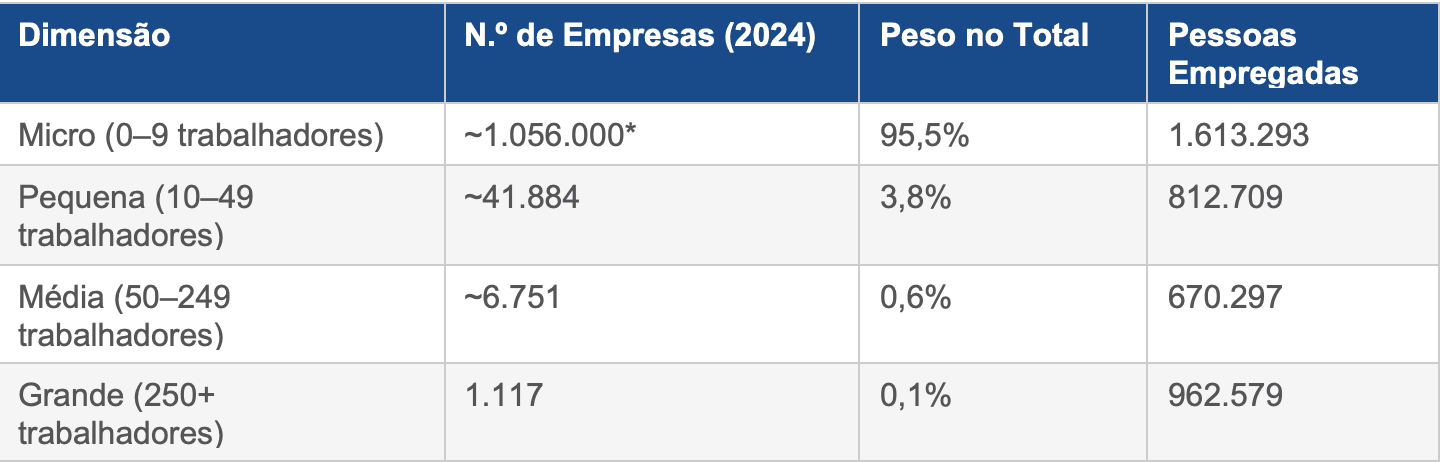

In 2023, Portugal had around 1.5 million businesses. Of those, 99.9% were SMEs. By 2024, the number of registered SMEs had grown to around 558,000, up from just 365,000 in 2006. That is a 53% increase in less than 20 years.

Here is how those businesses break down by size:

*Source: INE, European Commission SME Fact Sheet 2025, Banco de Portugal.

*Source: INE, European Commission SME Fact Sheet 2025, Banco de Portugal.

One interesting historical fact: Portugal has far more tiny businesses than most European countries. This goes back to 1974, when big private companies were broken up after a major political change. The result is an economy built almost entirely on small businesses, which makes the country very vulnerable when those small businesses struggle.

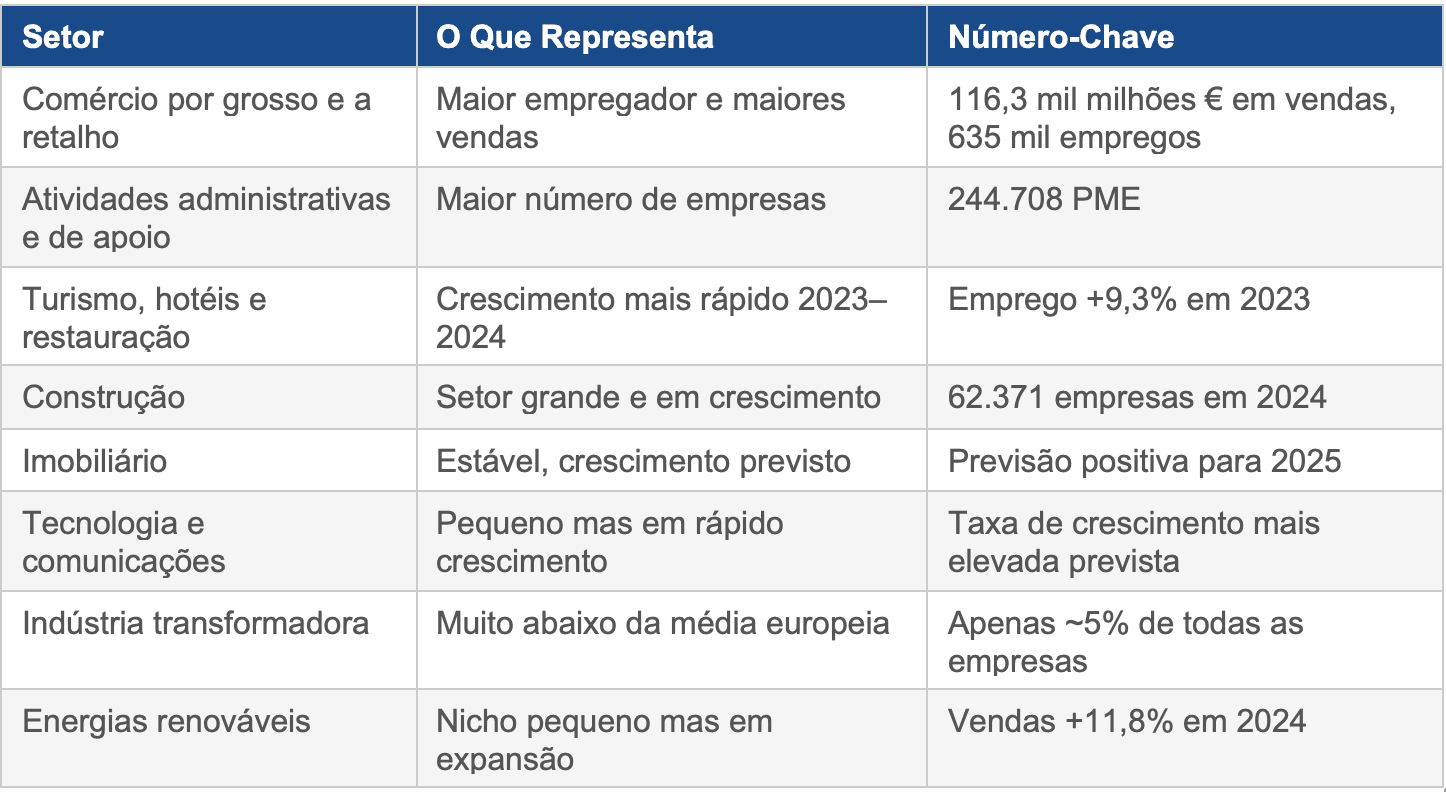

2. What Kinds of Businesses Are These?

Where are Portuguese SMEs concentrated, and what does that mean for their chances of survival?

Portuguese SMEs are spread across many different industries, but the pattern is telling: most businesses are in everyday services: shops, restaurants, cleaning companies, real estate agencies. Very few are in manufacturing or technology.

Why does the industry mix matter? Because the type of business you run affects how likely you are to survive. Restaurants and shops have very thin profit margins, meaning there is very little money left over after paying all the bills. They are also highly dependent on local customers spending money. When people tighten their wallets (during a recession, for example), these are the businesses that feel it first and hardest.

By comparison, tech companies and manufacturers tend to have more stable revenue, stronger profit margins, and customers spread across different markets. They are generally better at surviving tough times.

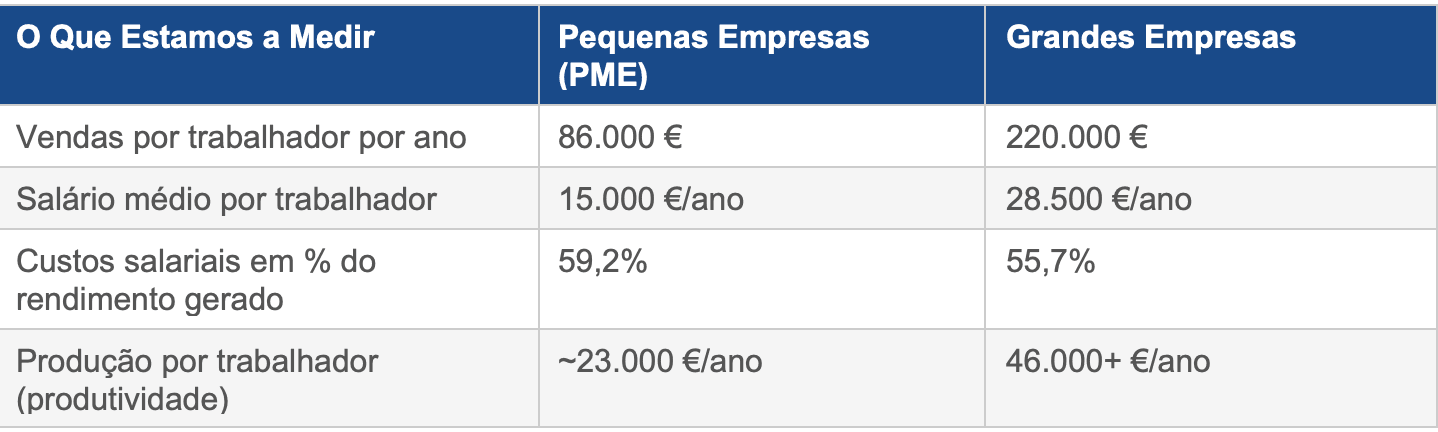

3. How Much Do These Businesses Earn?

SMEs generate most of Portugal’s economic output, but individual businesses earn far less than you might expect. Portuguese SMEs are responsible for about 68% of the country’s total economic output and employ 76% of all workers. That is higher than the European average, which shows just how much Portugal depends on its small businesses.

But when you look at what individual businesses actually earn, the picture is worrying:

In simple terms: employees in small businesses generate less money per hour worked, earn lower wages, and leave the business with less profit compared to large companies. A small business produces on average €23,000 of value per employee per year. The EU average is about double that.

Think of it this way: if a small business has 3 employees and each one generates €23,000 of value a year, that’s only €69,000 in total to cover all costs, pay everyone, and keep the lights on. There is very little room for error.

##4. How Long Do Businesses Actually Last?

The survival numbers are sobering. Let’s look at what they really mean.

Here is what the latest official data from Statistics Portugal tells us:

Por outras palavras: se abrir uma empresa em Portugal hoje, tem aproximadamente uma hipótese em duas de ainda estar ativo daqui a três anos. Não são probabilidades animadoras.

To put it simply: if you start a business in Portugal today, you have roughly a 1-in-2 chance of still being open three years from now. That is not a great set of odds.

In 2024, about 1.6 million businesses were active in Portugal. Around 247,000 new ones opened that year. But 187,000 also closed. The country is creating new businesses faster than it is losing them, but the individual survival rates remain very low.

Which industries are the most dangerous?

Not all businesses face the same risk. Restaurants, shops, and personal service businesses (like salons or cleaning companies) close at much higher rates than technology companies, professional services firms, or energy businesses. The pattern is consistent year after year: the businesses with the lowest profit margins tend to have the shortest lives.

How does Portugal compare to the rest of Europe?

Portugal’s 3-year survival rate of 47.7% is below the Western European average, which typically sits between 55% and 65%. The main reasons Portugal lags behind are: it is harder for small businesses here to borrow money, fewer businesses sell to customers outside Portugal, and most businesses are very small (which makes them more fragile). We will explore all of these in the next section.

5. Why Do Portuguese Businesses Fail?

Business failure is rarely one big disaster. It is usually a slow build-up of problems that were there from the beginning. Research consistently shows the same causes coming up again and again. External events: a recession, a pandemic, rising costs, are often what finally pushes a business over the edge. But the real problem is that most businesses were already fragile before those events happened. They had no cushion to fall back on.

5.1 Starting with too little money

Many Portuguese businesses start without enough money to get through the first year or two. The owner underestimates how much it costs to keep the business running before customers are paying reliably. When the bank won’t lend and there are no savings to fall back on, one bad month can be the end.

After the 2008 financial crisis, nearly 1 in 5 Portuguese SMEs that applied for a bank loan were rejected. When credit dries up and reserves are gone, there is nothing left to keep the business alive.

5.2 Difficulty getting a loan or financial support

Portugal consistently scores below the European average when it comes to small businesses being able to access loans and financial support. This is not just about banks being reluctant to lend. It is also about business owners not knowing what help is available, not having the paperwork to apply, or not having a clear enough financial picture to make a convincing case to a bank. There are EU and government programmes that can help (such as Portugal 2030), but many owners never use them.

5.3 Not investing in new ideas or better ways of working

Portugal’s businesses spend less on research and development than almost any other country in Europe, less than 1% of the country’s total economy. Businesses that do not improve or innovate tend to compete only on price, which squeezes their profit margins thinner and thinner. Eventually there is nothing left, and a cheaper competitor takes their customers.

5.4 Selling only to Portuguese customers

Most Portuguese SMEs have all their customers in Portugal. This is risky. If the Portuguese economy slows down, their entire business slows down with it. Businesses that sell to customers in Spain, Brazil, or other markets are much better protected because a bad year in one country does not kill the whole business.

5.5 Too much paperwork and tax

Running a business in Portugal involves a lot of administrative tasks: tax filings, compliance requirements, and bureaucracy. For a large company, this is manageable because they have staff to handle it. For a one-person business or a small team, it takes significant time and energy away from actually running the business. This is a common complaint among Portuguese business owners.

5.6 Owners who are great at their craft but not at running a business

A great chef is not automatically a great restaurant owner. A skilled builder is not automatically a great construction company manager. Many small business owners are experts in what they do, but have never been taught how to manage money, plan for the future, or build a team. This gap is one of the most common reasons businesses fail and one of the easiest to fix with the right support.

5.7 No cushion for tough times

The 2008 financial crisis wiped out thousands of Portuguese businesses. COVID-19 did the same in 2020 and 2021. The businesses that survived were the ones that had money set aside, manageable debt, and a plan. The ones that did not had no choice but to close. External crises are impossible to predict, but being financially prepared for them is entirely within an owner’s control.

6. The Money Mistakes That Kill Businesses

Of all the reasons businesses close, poor money management is both the most common and the most preventable. Here are the seven mistakes that do the most damage. A business can have a great product, loyal customers, and a dedicated team and still fail because the money is not being looked after properly. In Portugal, where profit margins are already tight, getting the finances wrong is rarely something a business can recover from.

Erro 1: Mistake 1: Thinking profit and cash are the same thing

This is the mistake that kills more businesses than any other. Here is the simple truth: just because your business is making sales does not mean it has money in the bank.

Imagine you complete a big job in January and send an invoice. Your client pays you in March. Your books show you made a profit in January, but in February, you still have to pay your staff, your rent, and your suppliers. If you spent the money you were expecting before it arrived, you are in serious trouble.

In Portugal, it is very common for large companies and government bodies to pay their bills late, sometimes 60, 90, or even 120 days after receiving an invoice. For a small business waiting on that money to pay its own bills, this can be catastrophic.

Profit is what your accounts show. Cash is what is actually in your bank account. You need to track both and understand that they are often very different numbers.

Mistake 2: Not knowing what money is coming in (and when)

Most small businesses in Portugal do not sit down and forecast their cash. They look at the bank balance when they need to make a payment and hope for the best. This works fine when business is good. It is a disaster when things slow down.

A simple cash flow forecast means writing down all the money you expect to receive in the next 3 months, and all the money you expect to spend. Without real-time cash flow visibility, you are always reacting rather than planning. Good cash flow management for small businesses also means tracking and categorising your business expenses properly, knowing exactly where the money goes is the only way to control it. Without expense tracking, your business is flying blind.

Once you forecast your cash and track your spending, you can see problems coming weeks before they arrive, giving you time to act. Without it, you only find out there is a problem when the bank account is already empty.

Think of it like checking the weather before going on a trip. You might still get rained on but at least you brought an umbrella.

Mistake 3: Mixing your personal money with your business money

This one is extremely common in Portugal, especially among sole traders and very small businesses. The owner uses the business bank account to pay personal bills. They take money out of the business whenever they need it personally. Business income pays for the family holiday.

The problem is that when everything is mixed together, you have no idea whether your business is actually making money or not. Proper invoice management becomes impossible - you cannot organise your business invoices, track which have been paid, or send documents to your accountant in any meaningful order. You cannot plan, you cannot apply for a loan (because your financial records are a mess), and you cannot see whether a quiet month is just normal variation or a sign that something is seriously wrong.

There is also a legal and tax risk. If the tax authority audits you, mixed finances can create big problems. It can put your personal assets at risk if the business runs into difficulty.

The fix is simple: open a separate bank account for the business and use it exclusively for business income and expenses. Organise your receipts and invoices by category from day one. Good document management makes accounting faster, cheaper, and far less stressful. Pay yourself a regular “salary” from the business account into your personal account. Keep everything else separate.

Here is something most business owners do not know: in Portugal, if you cannot produce the invoice for a business expense, that expense cannot be recorded in your accounts and you face a tax penalty of 50% of the expense value. Lose a €500 supplier invoice, and you could owe €250 in penalties on top of losing the tax deduction entirely. This is not a theoretical risk. It happens regularly, and it is entirely avoidable by keeping your invoices organised and safe.

A missing invoice does not just cost you the tax deduction. Under Portuguese tax law, it can cost you an additional 50% of the original expense value in penalties. Keeping your invoices is not optional. It is the law.

Mistake 4: Charging too little

Many Portuguese business owners charge less than they should. Sometimes it is because there is a lot of competition and they feel pressure to be the cheapest option. Sometimes it is simply because they have never sat down and calculated what it actually costs them to deliver their product or service.

Here is what owners often forget to include when they set their prices: the cost of their own time, the percentage of their fixed costs (rent, insurance, electricity) that should be covered by each sale, and a margin that allows them to make a profit and save for tough times.

If you sell below what it costs you to deliver, you will lose money on every sale. Selling more just makes the loss bigger. A business that undercharges will eventually fail. It is only a matter of time.

Mistake 5: Running the business without a financial plan

Would you drive from Lisbon to Porto without knowing the route? Probably not. But thousands of business owners run their businesses without any financial plan at all. No budget, no targets, no idea of what they need to earn each month to cover their costs.

Without a plan, every decision is made by gut feeling. You hire someone because it feels like you’re busy enough. You buy a new piece of equipment because you have some money in the account right now. You cut costs only when the bank account is already in the red.

A basic financial plan does not need to be complicated. It just needs to answer three questions: How much do I need to earn each month to cover all my costs? Am I on track to hit that number? If not, what am I going to do about it?

Mistake 6: Relying on your accountant to tell you how the business is doing

In Portugal, it is very common for business owners to outsource all financial awareness to their accountant. The problem is that accountants work on a reporting cycle and by the time they send you figures, those numbers can be up to three months old. You are essentially driving by looking in the rear-view mirror.

Knowing that your business had a bad January is useful information in January. Receiving that information in April, when the damage has already compounded, is too late to act on. Accountants are invaluable for tax compliance, legal structure, and year-end reporting. But they are not built to give you the real-time financial visibility you need to make day-to-day decisions. The solution is not to replace your accountant. It is to stop waiting for them to send you data. When you share invoices, receipts, and financial documents with your accountant in real time through accounting collaboration software, both you and your accountant are always working from the same up-to-date picture.

Many Portuguese owners only find out their business is in trouble when their accountant calls with bad news, news that was already visible in the numbers weeks or months earlier. By that point, the options are much more limited and much more painful.

Your accountant tells you what happened. You need a tool that tells you what is happening right now, and what is likely to happen next.

Mistake 7: Depending too much on one or two customers

If one customer accounts for more than half of your income, your business is at serious risk, even if that customer is paying on time and seems happy.

What happens if they decide to use a different supplier? What if they go through financial trouble and stop paying? What if they simply decide they do not need your services anymore? Suddenly, your entire business is in crisis through no fault of your own.

The more spread out your customer base, the safer you are. Losing one client out of twenty is painful but survivable. Losing your only major client can end the business overnight.

7. What You Can Do to Survive and Thrive

Most businesses fail for preventable reasons. Here is a practical guide to giving yours the best possible chance. The good news is that everything in the previous section is fixable. You do not need a finance degree. You do not need a big budget. You just need the right habits and the right information at the right time.

Step 1: Keep your business money completely separate from your personal money

If you have not done this yet, do it today. Open a dedicated business bank account and route all business income and expenses through it exclusively. Pay yourself a fixed amount each month as your wage. This one step makes every other piece of financial management possible.

Step 2: Know how much cash you actually have and what’s coming

Once a week, spend 20 minutes writing down what money is coming in over the next 3 months and what money needs to go out. Include your rent, wages, supplier payments, tax bills, and any big expected purchases. Compare that to your expected income. This is your cash flow forecast and it is the most powerful tool you have for small business cash flow management.

At the same time, track and categorise every business expense as it happens. Knowing your deductible business expenses, spotting where costs are creeping up, and being able to forecast upcoming spending are all things that only become possible when you have a live, organised view of your numbers.

Even a rough forecast that is 80% accurate gives you weeks of warning before a cash problem hits, instead of finding out when the bank account is empty.

The businesses that survive difficult periods are not the lucky ones. They are the ones who saw the problem coming and had time to do something about it.

Step 3: Know your key numbers off the top of your head

You should be able to answer these questions without opening a spreadsheet or calling your accountant: • How much do I need to earn each month to cover all my costs? • How much profit did I make last month? • How many days of expenses could I cover if no new money came in tomorrow? • How long does it take my customers to pay me on average? • Which part of my business makes the most money? Which makes the least?

If you cannot answer these, you do not have enough visibility of your own business. That is not unusual but it is dangerous.

Step 4: Build a cash cushion

The goal is to have at least 3 months’ worth of expenses sitting in your business bank account that you do not touch unless there is a genuine emergency. Getting there takes time, but once you have it, you can handle almost any normal disruption, a late-paying client, a slow month, a broken piece of equipment — without going into crisis mode.

Start small. Even putting aside a fixed amount each month builds the habit and the buffer over time.

Step 5: Make sure your prices actually cover your costs

Write down every cost involved in delivering one product or one hour of service. Include materials, your time, a fair share of your fixed costs (rent, insurance, phone bill), and the profit margin you need to grow the business. Your price needs to cover all of that, not just the obvious costs.

If your current prices do not cover everything, you need to either raise them or reduce your costs. Competing purely on being the cheapest is a strategy that almost always ends badly.

Step 6: Think before you spend

Before any significant expense - a new hire, new equipment, a bigger office, a marketing campaign- ask yourself three questions: Can I afford this right now without putting the business at risk? What will this earn me back, and when? What happens to my cash if this does not work as planned?

Businesses get into trouble not just from things going wrong, but from spending money optimistically before the income materialises to support it.

Step 7: Use tools that show you the full picture automatically

Keeping track of all of the above used to require a full-time accountant or hours of spreadsheet work. Not anymore. Modern financial management tools connect to your bank accounts and accounting software to give you real-time financial visibility, exactly where your money is, where it is going, and what is coming. They make invoice management simple, help you categorise business expenses automatically, and let you share documents and real-time accounting data directly with your accountant, so there is no more waiting three months for a report. They flag problems before they become crises and give you the information you need to make good decisions, without the complexity.

8. Final Thoughts

Portugal’s business community is bigger, more active, and growing faster than most people realise. More businesses are opening every year. Employment is growing. The outlook for 2025 is positive overall.

But behind those positive headlines, individual businesses are still closing at a very high rate. More than half of all new businesses will not be open in three years. Most of them will not close because of bad luck or a bad idea. They will close because they ran out of money, or because they did not see it coming until it was too late.

That is the hard truth. But it is also the hopeful truth, because these are problems that can be solved. The information, the habits, and the tools to manage a business’s finances well are all available. The only question is whether owners use them before a crisis forces the issue or after.

The most dangerous time for a small business is not during a crisis. It is the quiet period just before one. When the warning signs are already there in the numbers, but no one is looking at them.